As the dry market dropped off after the highs of last September, the underlying sentiment was that a resolution of the US-China trade war would provide a boost, driving up rates.

However, renewed concerns for the health of the global economy, spurred on by fears over the rapid spread of the coronavirus, have shaken the market, compounding worries that this could affect demand.

The past few weeks have shown a traditional plunge in the Baltic indices and a seasonal lull in the run-up to China’s lunar new year celebrations.

The Baltic Dry Index fell to a near four-year low of 539, well below levels seen in the same period last year in the wake of the Vale dam disaster.

The period market has also taken a hit, with rates for a capesize for one year down 14% from the start of the year to an average of $12,500 per day. Although we have come to expect a drop in rates at this time of year, the magnitude of this downturn is a surprise.

Reduced vessel supply

Last year, rates bounced back in the second half. Volumes recovered as Vale returned to the market faster than expected, and the impending IMO regulations reduced vessel supply.

Many capesizes left the market for scrubber installation, and with yards running behind schedule, vessel supply was cut further. Freight rates for the second half of the second quarter of 2019 were firmer overall, and six-month capesize time charter rates in the Pacific rose to $27,500 per day.

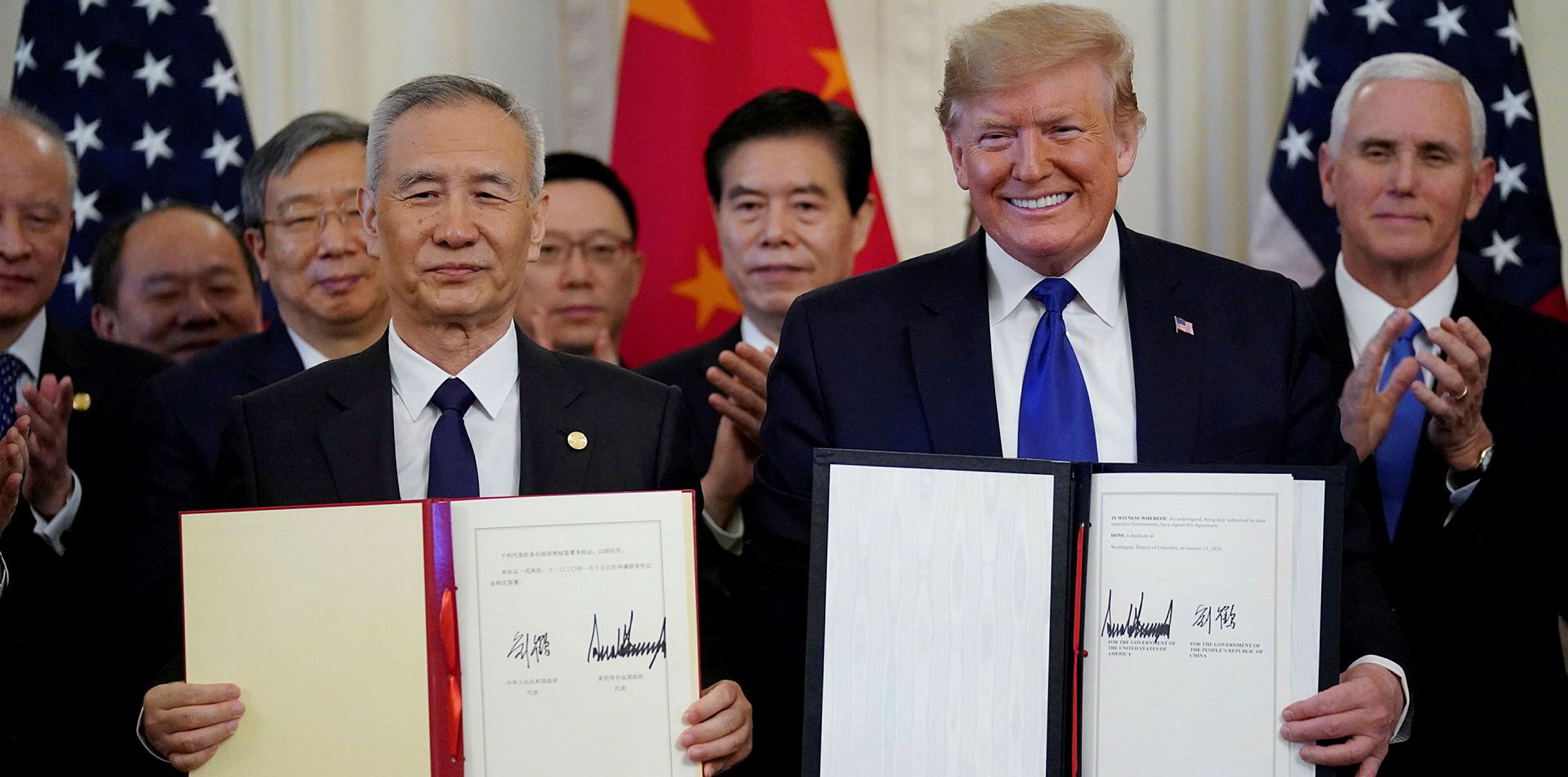

The signing of the phase-one agreement between Washington and Beijing — indicating the first steps towards a resolution of their long-standing trade war — should have given leverage to stimulate the economy after a period of uncertainty that has hindered growth in the dry bulk markets.

The agreement, signed on 15 January, specified that China will purchase an additional $32bn of US agricultural products until 2021.

However, the announcement has been marred by fears of the international spread of the coronavirus, creating short-term uncertainty for dry bulk demand.

At the same time, concerns persist surrounding the Chinese economy.

The latest World Economic Outlook from the International Monetary Fund again showed a downward revision of global economic growth for 2020 and 2021

The latest World Economic Outlook from the International Monetary Fund (IMF) again showed a downward revision of global growth for 2020 and 2021. Adding to the unease, GDP figures show that Chinese growth is at the lowest level in 29 years.

Trade war truce

Despite the truce in the trade war, the question remains as to whether the dispute has caused long-lasting problems for the Chinese economy.

The IMF expects that phase one of the deal, if durable, should reduce the cumulative negative impact of trade tensions on global GDP by the end of 2020 from 0.8% to 0.5%.

In the short term, worries surrounding the global economy are not good news for commodity and dry bulk demand. And the coronavirus could affect Chinese industrial activity, causing a ripple effect for dry bulk in the short term.

But despite this uncertainty, there is still scope for growth in the second half of this year and in 2021.

Rebecca Galanopoulos Jones is head of research at Alibra Shipping